The challenge of climate-friendly investing

If climate change is your main issue, building the right climate friendly portfolio is a struggle. We’ve looked hard and haven’t yet found an option that met both our financial and our ethical criteria. We documented the process. If you’re curious for the details, you can read our analysis of the landscape of climate-friendly investments options. Otherwise, here’s our high-level takeaways.

If you begin with an online search, you’ll come across a few investment platforms with a series of ethical investment portfolios. While their climate portfolios tend to hold great companies, they generally only have these companies in them. We found them a financially risky place to keep your life’s savings. Plus some have quite high management fees.

So you may look to the total market, ethical ESG ETFs from companies like Vanguard or Blackrock. These provide strong diversity and only modestly higher fees. As climate-focused investors, we struggle with ESG. Companies that score higher on Social (the S in ESG) and corporate Governance (the G in ESG), get included even if they have abysmal Environmental scores (E). So even though such funds are adequately diverse and have low-fees, they still invest your money in fossil fuel companies.

There has to be someone who has fixed this problem, right? There is, but be ready to pay a lot more for it. Mutual funds from ethically-driven investment companies such as Calvert and Parnassus do more ethical legwork to cut out questionable companies and will even engage in investor advocacy, but they are way far more expensive (up to 15x the cost of owning a Vanguard ESG ETF plus have high minimums). And, frustratingly, many still have fossil fuel companies in them.

How we build our stock portfolios

The stock market is composed of 11 broad sectors. These group companies together into sectors like healthcare, technology, and utilities. Our big “ah-ha” moment came when we realized that these sectors do a remarkably good job of grouping companies together based upon their carbon footprints.

Fossilfreefunds.org is a great tool for look up the carbon footprint of a mutual fund or ETF. If you lookup each sector, you will find that 84% of the CO2e emitted by publicly traded companies comes from only four sectors on the stock market: utilities, energy, materials, and industrials. What’s exciting is that in 2020, these four sectors only represented ~19% of the total stock market. That’s right, 85% of the CO2e pollution, only 19% of the stock market.

If you bought an index fund for each of the seven low-carbon sectors (technology, healthcare, communications, real estate, consumer staples, consumer discretionary, and financials), your portfolio would track 81% of the stock market while generating dividends from the companies responsible for only 15% of CO2e emitted by publicly traded companies.

From a financial perspective, this strategy grants exposure to 81% of the market, bringing a reasonable level of diversity. Plus their fees are lower than even the cheapest ESG funds. From an ethical perspective, cutting out the energy sector and the high-carbon sectors that support the fossil fuel industry, means there are truly zero fossil fuel companies in them.

What’s left are the sectors that do not depend on fossil fuels for their survival. When we transition to a decarbonized world pretty much all of these companies can adapt without changing their core business.

Low-carbon sector index ETFs

If you are unfamiliar with the term, an ETF (Exchange Traded Fund) functions similarly to a mutual fund, but generally costs less in fees and taxes.

In most mutual funds, fund managers buy or sell stocks regularly in an effort to “beat the market.” Because these managers are more active, they charge high fees. From a tax perspective, every time a manager sells a stock they held for less than a year, you have to pay short term capital gains taxes. This can get very expensive.

ETFs generally take a “set it and forget it” approach. A fund may be updated once/year. This results in lower management fees a lower tax burden.

Our portfolios hold no mutual funds, only ETFs. ETFs generally are based upon an external index that tracks a given part of the stock market. In our case, these indexes track the low-carbon stock market sectors.

There are three series of sector-based ETFs one can choose from: State Street’s, Vanguard’s, and Fidelity’s. So which do we use?

Well, state Street’s track only the largest companies in each category (those in the S&P 500) and has the highest management fees (0.13%), so we decided against it. That left, Vanguard and Fidelity’s sector funds, which are very similar. They use practically identical external indexes from MSCI and they each have more than enough under management to avoid any liquidity issues. So, given that Vanguard’s fees are slightly higher (0.10%) than Fidelity’s (0.084%), we opted for Fidelity’s set of sector ETFs. (You can checkout our full portfolio allocation)

Exceptions: financials and consumer staples

While sector-based ETFs are the base of our stock portfolios, there are two sectors that still have some companies that, we believe, do not belong in a climate-friendly portfolio. In the financial sector, these are the big banks and Berkshire Hathaway. In the consumer staples sector, these are the meat companies.

Big banks are profiting off of climate change. They do not belong in a climate-friendly portfolio. According to a 2020 report from the Indegenous Environmental Network, the top 6 US banks have funded 37% of fossil fuel expansionary activity since the Paris Agreement was signed in 2015. Chase is putting your savings account to work in oil fields.

Berkshire Hathaway, Warren Buffet’s holding company, owns the majority stake in multiple fossil fuel companies. These are not legacy positions. Berkshire Hathaway’s most recent fossil fuel acquisition was in 2020.

So instead of investing in the financial sector ETF, our portfolios hold two sub-sector ETFs that grant exposure to the sector without fossil fuels: regional banking and insurance. The regional banking ETF supports smaller banks who make money from traditional banking or providing loans to their members and smaller businesses. The insurance ETF holds insurance companies who make money from property, auto, and liability insurance.

Meat Companies not only profit from significant animal suffering, inequitable contracts with their farmers, and inhumane treatment slaughter-house employees, but they represent the beginning of the supply chain of an industry with a significant climate impact.

A 2018 study published in the journal Science surveying 37,800 farms across the globe found that even the lowest impact animal products are responsible for more CO2e emissions than vegetable substitutes.

So instead of investing in the consumer staples ETF, our software recreates the index without the meat companies. Our portfolios invest directly in the 89 individual companies within it at the same proportions, minus the meat companies (we also cut tobacco companies). The two meat companies (Tyson and Hormel) represented 1.63% of the consumer staples ETF. In our reconstruction of the ETF we gave their allocation to Beyond Meat, a vegan, meat substitute company (when other meat substitute companies go public [looking at your Impossible!], we’ll divide this allocation between them).

Replace high-carbon sectors with companies solving climate change

While cutting the high-carbon sectors (energy, utilities, materials, and industrials) from our stock portfolios effectively cuts the worst CO2e emitters, each of these sectors doe have companies that are working to do the opposite and solve climate change. From renewable power plant owners in energy, to wind turbine manufacturers in industrials, to battery makers in materials, there are many publicly traded companies that belong in a climate-friendly portfolio.

Unfortunately, the Fidelities and Vanguards of the world don’t offer a fund or index of all of the companies building climate solutions.

So we built one – the first ever index of publicly traded companies building solutions to climate change. We call it the Drawdown Index.

You can checkout the companies in the Drawdown Index and learn about how we built it. Our 2020 iteration has 112 companies.

To determine how much of the stock portfolio to allocate to a given company, we again, use the sectors of the stock market. It’s easiest to demonstrate this with an example:

- In mid-2020, the total market capitalization of the energy sector (all of the stock value added together) was $2.04 trillion.

- This represented 4.56% of the value in the total stock market.

- In the Drawdown Index, the energy sector has 10 companies in it of varying sizes. So, these companies split 4.56% of the stock portfolio in a manner proportional to their individual market capitalizations.

For more, you can check out our full portfolio allocation breakdown.

We’re fans of the Drawdown Index because we don’t believe simple fossil fuel divestment is enough – we need to invest in the future we want to see realized. In doing so, we increase the diversity of our portfolios while granting extra exposure to the companies solving climate change, helping them move just a little bit faster.

Exceptions: technology and consumer discretionary

While the majority of the companies in the Drawdown Index are from the four high-carbon market sectors, a few sub-categories of companies are not. LED, renewable energy software, and some telepresence companies are in the technology sector. Electric car companies are in consumer discretionary.

Rather than only getting exposure to these companies through their sector-ETFs, we wanted to also invest in them directly. So, we reserve 10% of the allocation meant for the technology and consumer discretionary sectors to invest directly in their respective Drawdown companies. An example: the technology sector represented 21.21% of the market in 2020. So we allocated 90% (19.09%) to the technology ETF and 10% (2.12%) to the Drawdown technology companies.

International stock funds: why we don't include them

Two reasons.

The first is ethical: we could not find any international ETFs that did not have fossil fuel companies in them (you can read more about our search for climate-friendly international equity funds).

The second is financial: we don’t believe you need to own international stocks to get adequate international diversification. You read more about our financial analysis on why you don’t need international equities, including why Jack Bogle, Vanguard’s founder, agrees with us. Here’s the high level argument: companies traded on the US stock exchange do ~50% of their business outside of the US anyways, so by investing in them you get exposure to international markets without the currency and political risk of owning stock traded on foreign exchanges.

The exception to this is in the Drawdown Index. There are a number of international manufacturing and utilities companies that trade on the New York stock exchange that met criteria for inclusion in the Index.

So that’s it! That’s how we build our climate-friendly, low-fee, diversified, market-tracking stock portfolios. We build the base of the portfolio with sector index funds that track 80% of the stock market. We then fill in the remaining 20% with the companies building climate change solutions in the Drawdown Index.

But what about bonds? Even the most aggressive stock portfolio should have some bond exposure be optimally balanced.

Choosing climate-friendly bond funds: green & fossil fuel free

There is something exciting growing in the world of fixed income: green bonds. These are issued by governments, municipalities, and companies to finance renewable energy and carbon pollution prevention infrastructure around the world. Because these types of projects are capital intensive but are profitable over time, they are ideal for debt-instruments such as bonds.

The core of our bond strategy is therefore built around green bonds. We personally want our money being put to work building this transitional infrastructure. There are two green bond ETFs currently on the market, one issued by Blackrock and one by VanEck. As the two have different underlying holdings, our portfolios hold both for maximum diversification.

The rest of our bond strategy is built around short, mid, and long term US Treasury bonds. We looked hard for other corporate or aggregate bond funds that did not hold bonds from fossil fuel companies, but could not find any. You can read about our full and ultimately futile search for the most climate-friendly bond funds.

One note: we do keep 1% of each Carbon Collective account in cash. A 80% stock, 20% fixed income portfolio will actually be 80% stock, 19% bonds, 1% cash. Keeping a small part of your accounts in cash reduces the potential tax burden from rebalancing – it decreases the likelihood our software will need to sell anything in order to rebalance.

How we build our safety net portfolio

While our general and retirement accounts are built around long-term investment goals with an eventual disbursement over time, our safety net/emergency fund portfolio is built for the opposite: to be fully liquidated at any point.

Therefore unlike the general and retirement, the safety net portfolio’s primary goal is capital protection with a secondary goal of capital accumulation. To achieve this, these accounts are very bond-heavy with 85% of them going to fixed income and only 15% to stocks. These accounts are highly risk averse, with 60% of the bonds in these accounts are in short term US Treasury bonds. You can check out our full safety net portfolio allocation.

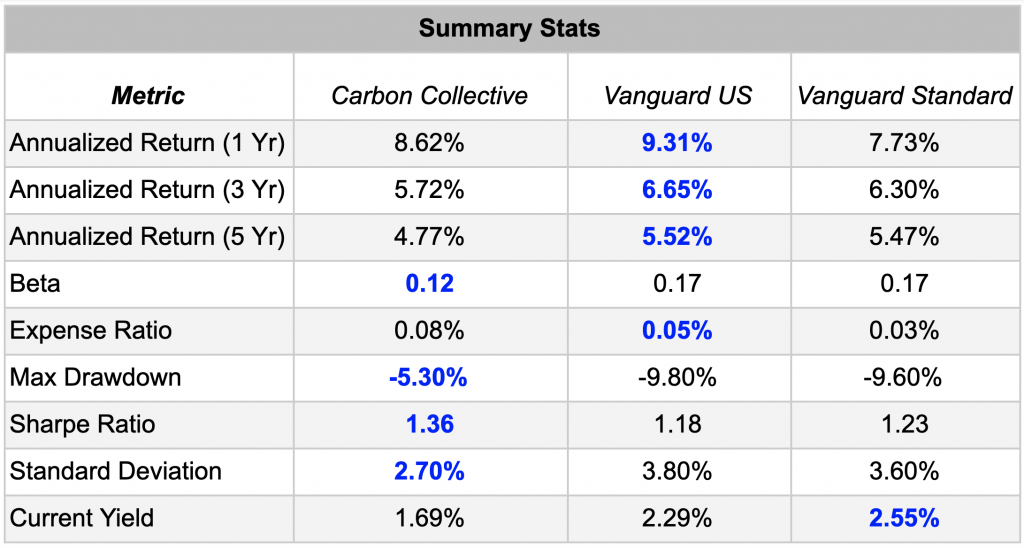

See the table below for some financial stats comparing our safety net portfolio to a comparable portfolio of Vanguard total market index funds. The five year time period is from 08/22/15 – 08/22/20. Read here for the full calculations.

While the Vanguard portfolio generated a better return over this time period, it was considerably more volatile, generating greater losses when the market went down, and had a stronger correlation to the overall stock market.

While the Vanguard portfolio generated a better return over this time period, it was considerably more volatile, generating greater losses when the market went down, and had a stronger correlation to the overall stock market.

Give special note to the standard deviation. This indicates that 95% of the time, we would expect this account to not suddenly lose more than 5.4% of its value.

Historical performance & financial stats

“Green” investing has had a historical stereotype of underperforming the rest of the market (and many have). So how did an investment strategy built using our climate-friendly strategy do?

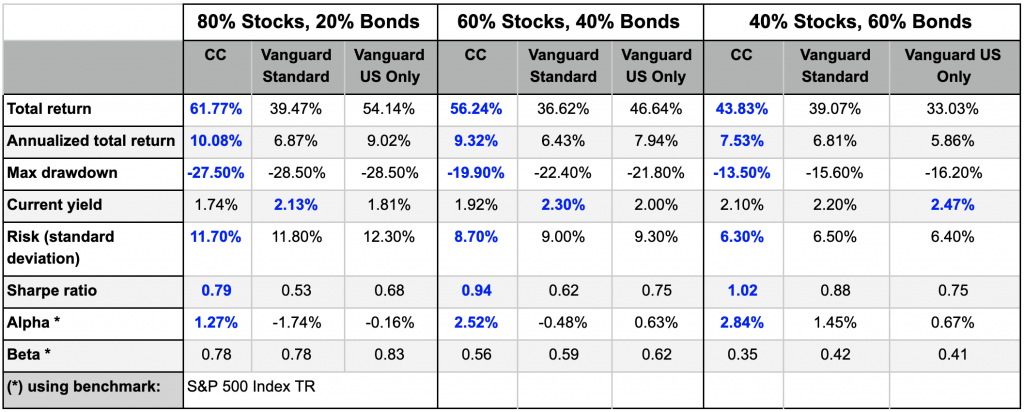

We ran three simulations to look back and see what would have happened if you had invested in three different Carbon Collective portfolios from 01/01/15 – September 1st, 2020 with annual updates at the end of each year. (Checkout the details of how we run simulations of historical performance).

We compared the results of each simulation with two benchmark portfolios both built with Vanguard index funds. The “Vanguard Standard” portfolio is a global portfolio built of four total market ETFs (US + Intl stocks, US + Intl bonds) and the Vanguard US Only has only two total market ETFs (US Stocks, US bonds). Again, for more details checkout how we ran the simulations.

Past performance is no guarantee of future returns, so what can we learn from this simulation? Across a series of portfolios, our climate-friendly strategy seemed to deliver moderately higher returns with lower risk. When the market fell in the Coronavirus downturn in Q2 of 2020, our portfolios fell less than their comparable Vanguard benchmarks.

All three portfolios had similar volatility levels compared to the S&P 500 (beta), with the Carbon Collective portfolios being slightly less volatile in the portfolios with greater bond exposure. A place the Vanguard standard portfolios have an advantage is yield, meaning their bonds generated higher interest and their stocks delivered greater dividends than Carbon Collectives. This makes sense as fossil fuel companies tend to distribute high dividends to their shareholders.

Will Carbon Collective’s portfolios continue to outperform? Who knows. Nobody can predict the future. What we can more confidently claim is that, at least over this time period, the stereotype of green investing underperforming the market did not prove to be true for our portfolios.

Conclusion

From the outset, our goal was to build investment portfolios that met our financial and climate standards. We basically wanted them to be just as diverse and low-fee as index funds but without fossil fuels and supporting the companies solving climate change.

We did that by focusing on the CO2e emissions of each stock market sector, buying index funds of the seven sectors with low carbon footprints and replacing the high carbon sectors with direct investments in the companies in those sectors building climate solutions. For our bond portfolios we replace corporate with green bond funds and balance the rest with US Treasury bond funds.

We would argue we hit our goal. Simulating a portfolio as if you had adopted this strategy in early 2015, you would have gotten a similar (likely better) performance than a standard index-based portfolio while still largely tracking the overall market. All in a portfolio with a 94% lower carbon footprint that also directly invests in 112 companies solving climate change and costs the same in management fees as most index-based portfolios.

If you’re like us, and you want your investments supporting and betting on the companies solving climate change, rather than making it worse, check out our climate-friendly investment platform.

And yes, it’s where we keep our retirement accounts🙂