Our financial philosophies

There are many ways to build an investment portfolio. The public markets have tens of thousands of stocks, bonds, mutual funds, ETFs, commodities, (etc.) that you can invest in. There are countless permutations of how you can put them together.

At the same time, the personal finance industry and related academics have studied which strategies tend to do better than others. Their findings are no guarantee of the future. There are pretty much no certainties when investing. But they offer some clear guidelines of what has historically worked best for long term investors.

We want to share the philosophies we use to build our climate friendly portfolios at Carbon Collective.

Track the market wherever possible (index funds)

Some people like to choose stocks and bonds themselves when investing, but many (including us) prefer to buy pre-built collections of them. In general, these collections come in two flavors.

Actively managed funds have a goal to “beat the market.” The fund managers actively buy and sell stocks as the market changes. If they are successful, the returns on investing in their mutual fund will be higher than those of the overall stock or bond market. Generally, actively managed funds are structured as mutual funds.

Index funds often have a goal to passively “track the market.” The fund managers will choose an underlying index like the S&P 500 or the technology sector, and put together a collection of stocks or bonds that will track the performance of that category. They will only buy or sell stocks or bonds within the fund occasionally, like if a new company emerges in that category. Generally, index funds and passively managed funds are structured as Exchange Traded Funds or (ETFs).

So which type of fund works better?

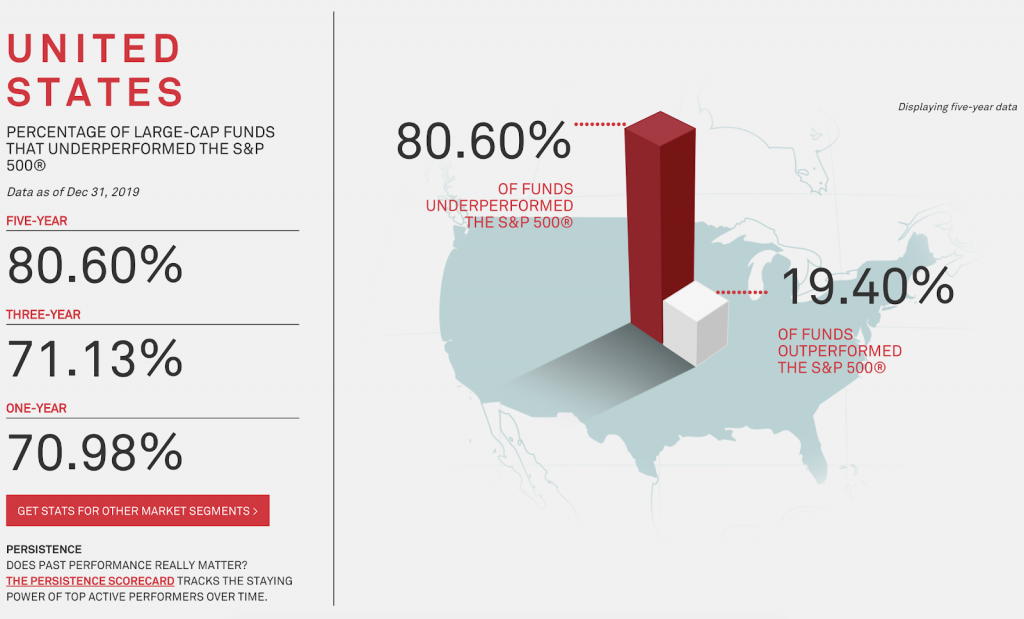

While there are no certainties when investing, index funds have historically been a general smarter investment strategy than actively managed funds.

Why is this true? You would think that over the decades, fund managers would get better, to the point that maybe 50% of actively managed funds would outperform the overall market.

- It’s really hard (impossible) to consistently predict the future. As humans, we are prone to optimism bias. We tend to believe negative outcomes are less likely to happen to us than their actual statistical likelihood. Let’s make one thing clear. This bias can be a major positive. It helps us push through fear in taking a risk to live out a dream. How many amazing novels, businesses, medicines, and songs wouldn’t exist without optimism bias?

But in the world of public stock markets, optimism bias enables both a mutual fund manager and an investor to both believe that they will be the exception to the rule. Optimism bias pushes us towards focusing on that 20% of funds that did outperform the general market. What if I had invested in those?

The problem is, there is no evidence that funds that outperformed the stock market over the last five years will outperform it over the next five years. Burton Makiel named this Phenomenon “A Random Walk Down WallStreet.” Looking at the data, he argues that you will have equal luck using a blindfold and a dartboard vs. using historical performance when trying to pick a strategy that will “beat the market.”

- They charge much higher fees. But if it’s random, shouldn’t actively managed funds outperform the market about 50% of the time? Before fees, it’s much closer. The problem is actively managing a fund takes a lot more work. And this work needs to be compensated.Actively managed mutual funds can charge fees that are up to 20x higher than a passively managed ETF. These fees can often erase any gains a fund manager was able make against the market. So many actively managed funds can’t just beat the market by a little bit. They need to beat it by enough to cover their much higher fees.

So, wherever possible, we use passively-managed index funds. Where we can’t just adopt an index fund because they don’t meet our ethical standards for climate-friendly investing, we try to emulate a passively managed index fund.

Instead of investing in an energy-sector index fund which is almost all fossil fuel companies, our portfolios hold that spot open for renewable energy companies. And not just the one we believe will perform better, but all of them. We get your savings invested in the entire category of renewable energy.

Diversify, diversify, diversify

You may have heard this investment advice before? But what’s the rationale behind it?

There are two major reasons to diversify your portfolio.

The first is pretty simple to understand. It’s essentially the adage: “don’t put all your eggs in one basket.” The more you diversify your portfolio the more you protect against the risks of any individual investment failing from risks that are specific to that company. These could include fraud from the management team, congress passing legislation against its industry, or the company is simply beaten by competitors.

In general, these type of company and industry specific risks are called unsystematic risks. The more categories your portfolio touches on, the more you can diversify away these risks.

For our portfolios we address unsystematic risk by diversifying across the entire stock market. Even though we cut out the high-carbon sectors entirely like energy, we reintroduce the climate-friendly alternative, like renewable energy companies, to grant exposure to the sector.

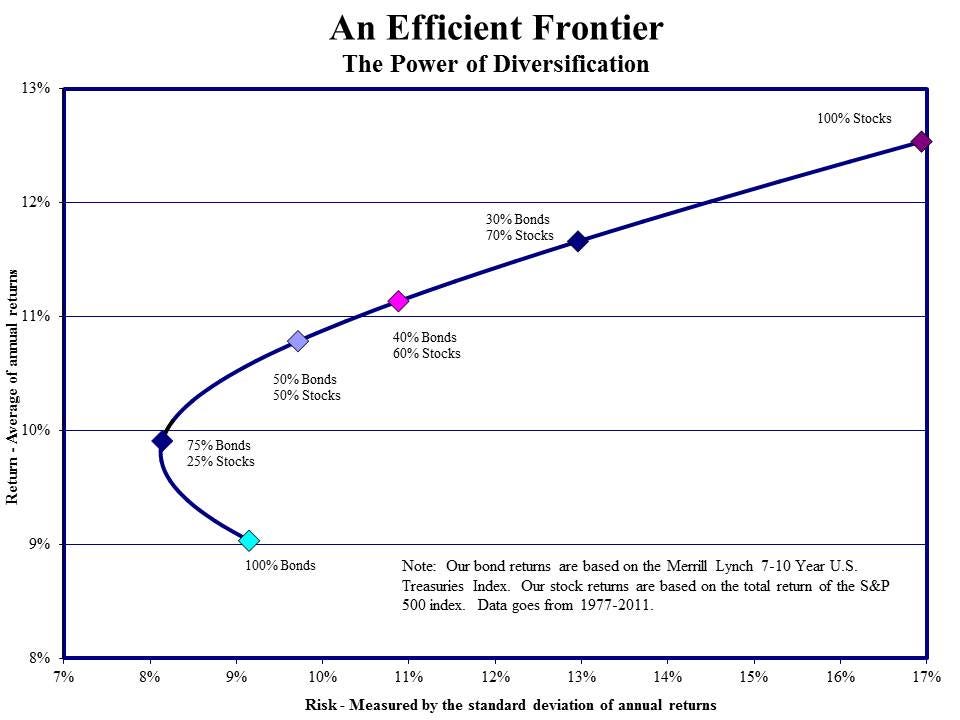

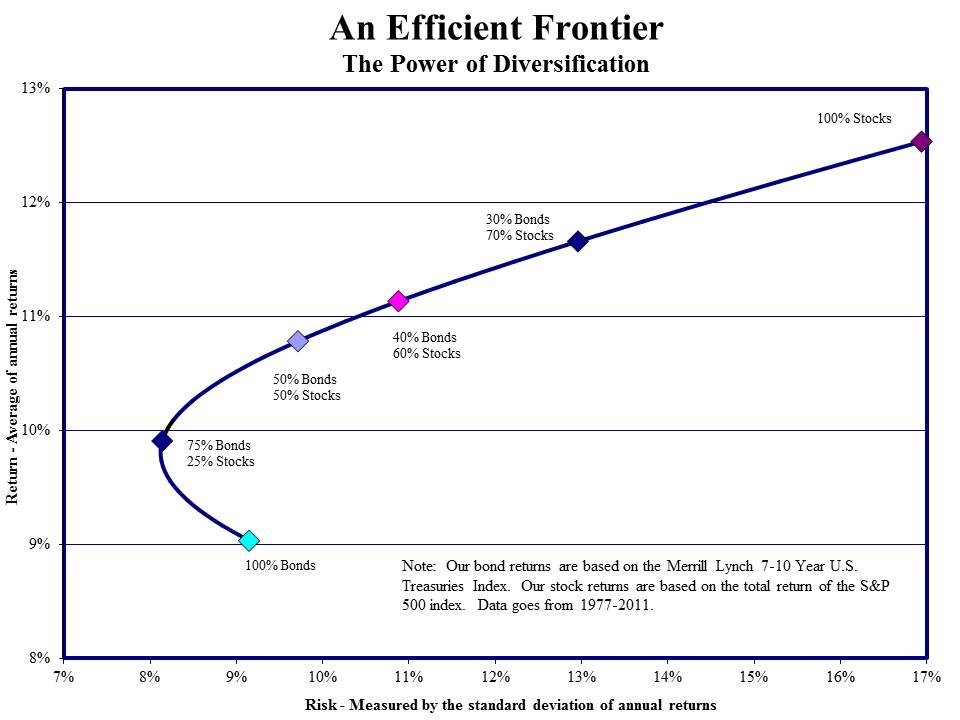

The second is a bit harder to grok and it’s all about correlation. In 1952, an economist named Harry Morkowitz studied the risk and return profiles of different mixes of investments.

What he found changed the world of investment forever. In general, the only way to generate a higher investment return over the long run is to take on more risk.

This rule is largely true, but Markowitz presented the exception. A properly diversified collection of investments that have a low correlation to each other, can achieve a higher expected return with a lower expected risk.

Stocks and bonds have fairly low correlations. The value of stocks is dependent on a number of factors including investor confidence where the value of bonds is largely determined by the interest rates set by the federal reserve. If you invest in bonds, you are much less likely to lose money, but the upside is also much lower.

You would think that an investment of 100% bonds would carry the lowest risk (and lowest return). But that’s not the case. Mixing bonds with a poorly correlated investment, like stocks, generated a higher return with less risk.

Look at the graph below which studied portfolio mixes over 40+ years on the stock market.

Markowitz named this revelation Modern Portfolio Theory, which often gets shortened to MPT. How does it work? If you’re interested, here’s a corny, but helpful walk-through video of the math.

We balance our stock portfolios with green and government bonds that have low and negative correlations to the overall stock market. See the chart below on how the bond funds we use correlate with the overall stock market. VOO = S&P 500. VTI = Total US Stock Market.

- The two green bond funds, BGRN and GRNB, have moderate correlation (purple cells on the bottom left)

- The short, mid, and long term US treasury bonds (VGSH, SCHR, VGLT) all have a negative correlation with the overall stock market (green boxes)

- The inflation protected bond (STIP) has a moderately high correlation with the stock market, but a negative correlation with the other bond funds.

Choose ETFs with the lowest fees

Our portfolios only use ETFs, rather than mutual funds. They tend to have lower fees, tax burdens, and generally better fit our goal for investing in index funds.

When you’re looking at index fund investing, there are multiple ETFs you can choose from in each category. For sector-based index funds, for example, you could choose a technology sector ETF from Fidelity, Vanguard, or State Street.

For our portfolios, we ask ourselves three questions when choosing an ETF:

- Does it closely track its underlying index?

- Does it have enough money invested into it to avoid liquidity risk?

- Does it have the lowest fees?

Often there are multiple ETFs to choose from that both closely track their underlying indices and have enough money under management to avoid liquidity risk. In these cases, we then choose the ETF with the lowest fees.

For example, our climate friendly stock portfolios are primarily constructed with sector-based index ETFs. Vanguard and Fidelity both offer comparable ETFs, but Vanguard’s cost 0.10% per year and Fidelity’s cost 0.084% per year. Therefore, our portfolios use Fidelity’s ETFs.

Conclusion

To summarize, the tenants of smart investing for the long term is not complicated. Don’t try to beat the market. Instead, invest in entire categories of stocks or bonds using index funds. Generally, ETFs will be more cost-effective than mutual funds.

Diversify your portfolio to make sure some of your investments have low correlations with each other. This will protect your investments from falling too far when the market turns, making it easier for it to recover.

If all else is equal, invest in ETFs with the lowest fees possible.

These are the strategies we use to construct our climate friendly portfolios. For about the same cost as investing in a portfolio of traditional index funds, you get broad diversity with exposure directly to 81% of the stock market plus direct investments in the 112 companies solving climate change. Instead of corporate bond funds which all contain bonds from fossil fuel companies, your savings get put to work building green infrastructure in green bonds around the world.