Periodic maintenance - portfolio rebalancing

The stock and bond markets change over time. Sometimes they lose value sometimes they gain value. Each of these changes impact the overall makeup of your portfolio. If the stock market is doing really well, the stocks in your portfolio will rise as well, taking up a greater percentage of it. Same for bonds.

The purpose of regular maintenance with portfolio rebalancing is to do small changes to keep your portfolio aligned on its goals.

Let’s dig into the details.

What is portfolio rebalancing

Let’s say you are saving for retirement. You don’t expect to retire for 30 years, so it’s a long time horizon. Also, you are comfortable taking risks with your money. You can sleep at night even if your portfolio were to suddenly drop significantly.

In general, the longer term your goal and the higher your risk tolerance, the more of your account will be in stocks and vice versa for bonds. So, we’d likely put this retirement fund in our most aggressive 90% stock, 10% bond portfolio.

Let’s say after six months, the stock market has done really well. The value of your stocks has increased to the point that the stocks now represent 95% of your portfolio. This pushed your overall portfolio out of balance, it’s now too risky. So what happens?

We rebalance it. If there is any extra cash in the account, we’ll use it to buy more bonds to increase its % of the portfolio. If that’s not enough to get back within the target % for your account, we’ll sell some of the stock and use the proceeds to buy more bonds (actually our software will do it automatically).

This process is known as portfolio rebalancing and it’s one of the biggest benefits you get from working with an investment advisor over handling investments yourself.

Why portfolio rebalancing is important

It’s important to rebalance a portfolio for two reasons.

1) It keeps your portfolio aligned to its goals. This is especially true when you’re going to start withdrawing money from an account soon. If your account is very conservative, a stock market boom could leave your account too exposed to a stock market drop. Rebalancing would enable you to capture the gains from the stock market boom by keeping them in a much more conservative investment: bonds.

2) It’s historically led to better historical performance.

The reason is pretty straightforward: rebalancing often leads to “buying low and selling high” in your portfolio.

Let’s go back to our retirement account example. The stock value increased over those six months from the original investment. The bonds may have increased as well, depending on the kind, but not as much. It is likely they may have even decreased in value as many bonds, US treasury bonds in particular, are negatively correlated with the stock market.

In automatically rebalancing, you’ll capture some of the gain from the rise in value of your stocks by selling a portion of them. You’ll then use the proceeds to buy more bonds, which may be trading lower. The vice versa is also true in times when the stock market goes down. Selling bonds to buy more stocks, positions your account to capture the stock market gains when the market recovers.

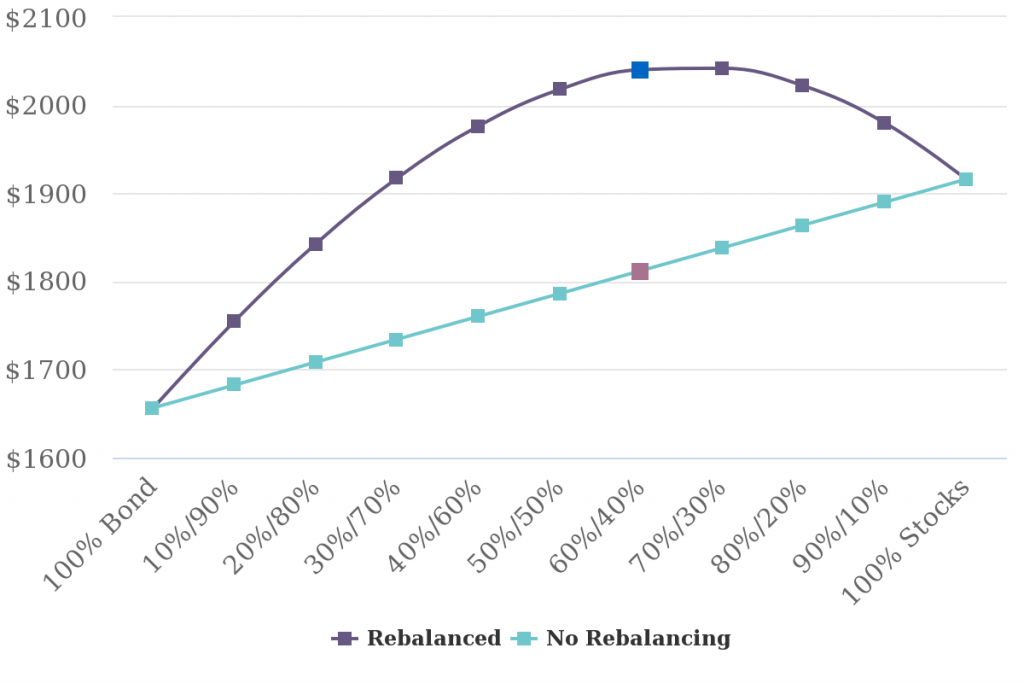

Morgan Stanley illustrated this phenomenon with a very basic investment portfolio combining the S&P 500 index and the US Barclays aggregate bond index. They ran a historical simulation that looked at what the value of a $100 investment would be from 1977 – 2014.

Generally, the higher the risk, the higher the reward, so you would expect a portfolio of 100% stocks to outperform the rest, particularly over such a long time period. This was true without rebalancing.

But the best performing portfolio was made of 60% stocks, 40% bonds, and got regularly rebalanced. This makes sense. There were stretches during this period where bonds did better than stocks (such as during the 70s and after the tech bubble). By keeping a sizable portion of these portfolios in bonds, it helped these portfolios hold value during these downturns.

Portfolio rebalancing - what you can expect

We use a trigger rebalance for accounts managed by Carbon Collective. Our software will automatically rebalance a part of your portfolio if it goes beyond 25% of its original target allocation.

Let’s look at an example.

Let’s say a technology sector ETF represents 22.3% of your total stock portfolio.

If things change pretty dramatically and it goes beyond 25% of its original allocation (lower than 16.73% or higher than 27.88% for the example above), it’ll get automatically rebalanced to back within 25% of the original allocation.

The software tries to limit selling something whenever possible to avoid unnecessary capital gains taxes. We always keep 1% of your account in cash to have something liquid.

As your investments generate cash of their own from interest and dividends, our software will use any cash in excess of 1% of the portfolio to keep your account balanced.

If there is not enough cash in the account when rebalancing is required, it will sell something to free up the necessary cash. In our technology ETF example, it might end up needing to sell some shares of the ETF if it was above 27.88% in order to free up cash to buy more shares in our green bond funds.

Do you ever need to do anything to rebalance your account?

Nope. You never need to worry about rebalancing. Our software handles it all for you in the most tax-efficient manner possible.

Annual portfolio maintenance

Aside from automatic rebalancing, there aren’t any other changes we’ll be making to your portfolios on a day to day basis. The goal is to help you “stay the course”

But, to continue the analogy, there are times when it’s important to take out the map, check the wind, and make adjustments. There are a series of checkups and updates that we’ll be doing on your account on an annual basis. Let’s walk through them.

Do the sector still match the total stock market?

Our climate-friendly stock portfolios are built to track the total stock market, like an index fund, but with the high-carbon sectors replaced by the companies solving climate change.

There are 11 stock market sectors. In the beginning of the year, we allocate the percentage that each gets in your portfolio based upon its current size in the market. If the technology sector represents 22.3% of the total market, then we allocate 22.3% of our stock portfolios to it.

As things change in the market over the year, the allocation in your portfolio might rise or fall. If things change pretty dramatically and it goes beyond 25% of its original allocation (lower than 16.73% or higher than 27.88% for the example above), it’ll get automatically rebalanced to back within 25% of the original allocation.

After the year has passed, we’ll update the target allocations for each sector to match the latest conditions of the market. Technically we do this at least one year and a day later to avoid any unnecessary short term capital gains taxes.

Do companies need to be added or removed from the Drawdown Index?

When we update the market sector’s allocations, also refresh our collection of all of the companies solving climate change. We cut any companies that no longer meet our standards for inclusion in the Drawdown index and added new ones that made the necessary changes to meet these criteria. If new companies have come onto the market that meet criteria, we add those as well.

We built the Drawdown Index to always be a work in progress. If you have comments, questions, or concerns, we want to hear about them. If you think we missed a company, or we made a mistake by including a company, please let us know at drawdownindex@carboncollective.co. We’ll take them into consideration (and likely reach back out to you to get your further thoughts) during this annual update.

Are there new funds that would make our portfolio substantially more diverse?

This is unlikely to often happen, but it’s worth calling out. In some categories, we may add new funds to increase diversity during this annual update.

The area this is most likely to occur is green bonds. Currently there are two green bond ETFs. We include both because they have relatively little overlap in their underlying bonds, so it’s a good way to get more exposure to the green bond ecosystem.

If a third green bond fund emerged and met our financial and ethical criteria for investing and it had little overlap with the other two funds, we would consider adding it to our portfolios to increase their diversity.

Conclusion

Once you onboard with us at Carbon Collective, all of the hard work is behind you. If there are big changes in the market, we’ll keep your accounts balanced and focused on your goals.

Every year, we’ll update all of our portfolios to reflect changes in the market. We’ll update the allocation for each stock market sector, refresh the Drawdown Index, and occasionally add a new fund to our portfolio to increase its diversity.